Demystifying Carbon Negative/Neutral, Climate & the Oil Price Crash of 2020

The newsletter for independent thinkers on carbon and climate.

What’s the difference between carbon negative and carbon neutral?

It’s getting hard to read the news without coming across a company promising to “reach net zero” or go “carbon neutral” or even become “carbon negative.”

Mining company Rio Tinto and airline Delta are among the latest companies announcing plans to go carbon neutral, while Amazon, Apple, Tesla and other tech giants are all committed to dramatically reducing their carbon footprints.

So what do all the different pledges mean and how can you compare them?

Net zero, carbon neutral or carbon negative?

Here is a list of definitions to help you navigate the wave of corporate green pledges:

Net Zero: Net zero means that any carbon dioxide released into the atmosphere from the company’s activities is balanced by an equivalent amount being removed.

Carbon Neutral: Carbon neutral is slightly different, allowing companies to measure the amount of carbon they release and offset that with a reduction in emissions or a removal of carbon. This can include buying carbon credits to make up the difference, making it appealing to companies that produce a lot of emissions.

Carbon Negative: The next step – becoming carbon negative – requires a company to remove more carbon dioxide from the atmosphere than it emits.

New pledges, new responsibilities

The United Nations says climate change is the defining issue of our time and without drastic action, adapting to the changes it will bring will be difficult and costly.

Companies are in the spotlight since studies show they’re responsible for the lion’s share of greenhouse gas emissions, creating a blanket of gas that traps heat and raises Earth’s temperature.

Amazon’s corporate carbon footprint alone – measured as the total greenhouse gas emissions attributed to its direct and indirect operational activities – rivals that of some small nations.

In the past, some companies have been accused of “greenwashing” – or overstating their eco credentials to garner favorable publicity. Companies have also been accused of setting headline-grabbing goals that look too far in the future and aren’t measurable.

But for many companies, the narratives have changed, acknowledging the need to find long-term solutions that create real impact.

The Microsoft Way

“It won’t be easy for Microsoft to become carbon negative by 2030,” Brad Smith, Microsoft’s President

Microsoft recently announced a detailed plan that it says is grounded in science and math, alongside interim goals spelling out how it plans to get there.

The company has promised to become carbon negative by 2030 and, by 2050, remove all of the carbon the company has emitted since it was founded in 1975.

This is a bold bet – a moonshot – for Microsoft. And it will need to become a moonshot for the world. LINK

Issue No. 18

Welcome to the latest issue of Carbon Creed! Last week our top two articles were Why don’t we panic about climate change like we do coronavirus? & Europe just had its warmest winter since at least 1850

My name is Walter McLeod, and I’m glad you’ve joined our tribe. We hope to hear from you as we navigate this weekly journey through the good, bad and ugly of carbon and climate. You can ping me anytime at mcleodwl@carboncreed.com.

If you are a subscriber, THANK YOU, and please share this to a friend.

If you haven’t subscribed, GIVE US A TRY, you can opt-out at anytime.

Now, LET’S GO DEEP!

GOVERNMENTS

Christine Lagarde, president of the European Central Bank (ECB), chats with Mark Carney, governor of the Bank of England, at the launch of the COP26 Private Finance Agenda in London on Feb. 27, 2020. (Photographer: Simon Dawson/Bloomberg)

Finance Can’t Decide How It Wants to Deal With Climate Change

Many financial managers see climate change as an opportunity, as expanding into services and products that claim to take it into account is a way for active investment managers to rise above the stiff competition posed by cheaper passive index funds. These products tend to bear the “environmental, social, and governance” label, indicating they’re not just good investments, they’re good investments. Larry Fink of BlackRock Inc., explaining in January why the world’s biggest asset manager would incorporate ESG principles into more of its products, indicated that simple customer demand was the main rationale.

Meanwhile, government officials working on mitigating climate change are putting the financial sector at the forefront of efforts to corral the international community into helping. The U.K., which is scheduled to host the United Nations’ annual climate change meeting in November, has chosen finance as a key element of its diplomacy before the summit. Mark Carney, the outgoing Bank of England governor and former chair of the G-20-linked Financial Stability Board, is assuming not one but two climate-related roles: UN special envoy on climate action and finance, and the U.K. prime minister’s finance adviser for this year’s climate meeting, COP26.

This effort to put finance at the center of the climate conversation partly reflects a hope that the capital markets will be faster and more rational than political bodies, where efforts to arrest climate change have tended to struggle and languish. Consider how many experts and commentators have said China’s authoritarian model appears to be more effective at managing emissions than most democracies; if we’re looking for alternatives, the capital markets might be better than authoritarianism. Carney’s speech launching the U.K.’s COP26 “private finance agenda” on Feb. 27 encapsulated that logic. “The objective for the private finance work for COP 26 is simple,” he said. “Ensure that every financial decision takes climate change into account.”

Are we trying to protect the climate with finance, or protect finance from a changing climate? It’s a question that gets discussed surprisingly rarely considering how important climate change is becoming to finance and vice versa.

On top of being a risk to individual financial assets, climate change is a risk to the entire financial system. It seems reasonable to believe the all-powerful market could help ward off this threat. Bringing climate change into financial decisions, however, is not necessarily the same as finance taking action to address climate change. That might sound obvious, but it’s not unusual to be at a panel discussion or roundtable about climate finance and hear some participants speak in the narrow sense of risks and returns while others talk about limiting climate change broadly.

BlackRock, now seen by many as a climate champion after its embrace of ESG criteria, published its own view of such official taxonomies in January. The document cautions against being “overly prescriptive” or imposing “binary definitions” and makes frequent reference to ESG financial concerns as materially important. In other words, BlackRock is taking the Mark Carney approach: Climate and social considerations should be central to investor decision-making, but the objective is purely financial, not climate-related.

As concern about climate change grows, and as marketing of “sustainable finance” products ramps up, it may be customers—both retail and institutional—and policymakers who have the final say. At some point, the great and the good in climate diplomacy and the financial sector will need to be much more frank about whether their goal is to protect the climate or investment returns. LINK

CLEAN TECH

3 hard-won lessons from a decade of negative cleantech returns

Two crucial weapons that can help us combat global warming are innovation and environmental regulation. Innovation pushes the market to become less oil-dependent and more environmentally friendly. Regulation, on the other hand, forces companies to invest capital, and to further reduce their carbon emissions.

One of the critical forces that encourages innovation is the venture capital (VC) industry, which has traditionally tried to avoid interacting with regulators. Not all investment sectors are created equal, however, as VC pioneers in the energy sector have discovered over the past decade of clean-energy investments.

In the decade prior to 2016, energy-related VCs lost more than half of their investments - that's around $12.5 billion. Only in recent years have the survivors of that financial carnage been able to learn from the mistakes of the first movers, gaining the sophistication required to succeed in this challenging field.

Today, after a decade of failures, the clean-technology industry's maturity has finally reached an inflection point. The VC sector can benefit greatly by learning three lessons from their experiences; the search for capital efficiency, the need to understand the regulatory landscape, and the need to play in rapidly growing markets.

1.Energy investments are inherently prone to capital intensity - which means that in many cases, they require a lot of capital expenditure before revenues begin to appear. This is mostly a result of the need to develop energy-related hardware before a company can start the sales process. For that reason, to successfully encourage VC-led innovation, there is a need to focus on software-based, capital-efficient investments. Capital intensive, hardware research and development investments like energy capacity technologies should be left to corporations who can commit to multi-year research and devlopment budgets without seeing returns or to funds that have very specific hardware expertise.

2.In energy, regulation matters. Energy is a field that, in some crucial respects, is led by regulatory reforms such as carbon mandates, carbon taxes, energy rebates and emission goals, to name but a few. The ability to sell to regulated utilities poses a challenge that not every start-up can handle. This means that VCs who wish to succeed in the field need to both understand the way regulations develop and be able to help entrepreneurs deal with sales to power stations and transmission companies. One great example is the $465 million government loan that saved Tesla at a crucial time. Without great VCs advocating for Tesla within the government, some say the company wouldn’t have been able to make it.

3.Not all fields and technologies within the energy sector grow in the same manner. Some areas, such as electric vehicles and energy storage, have experienced double and even triple-digit growth. At the same time, other sectors - such as internal combustion engine-driven vehicles - are in decline.

The cleantech investment industry is at a critical time in its history. VC investors should implement these hard-learned lessons to accelerate the transition to a cleaner future - one start-up at a time. LINK

INSIGHTS

What the Oil Price Crash Means for the Climate

For those awaiting more aggressive action on climate change, it may look like a breaking point has finally arrived.

A sudden collapse in fossil-fuel markets akin to the 2008 financial crisis has long been a scenario for how the world switches to a less carbon-intensive path. With Brent crude trading near $30 and the average yield on the U.S. energy sector’s junk debt above 15% — nearly double its levels in mid-January — it looks very much like a credit crunch is upon us.

At the same time, there’s reason to be fearful. Russia’s finance ministry has said it could sustain oil prices below $30 for as long as a decade. Setting aside a brief dip in the late 1990s, dollar crude hasn’t been at those levels in real terms since the 1973 oil crisis. In theory, that should be bullish for consumers of oil and bearish for purported substitutes, such as electric vehicles.

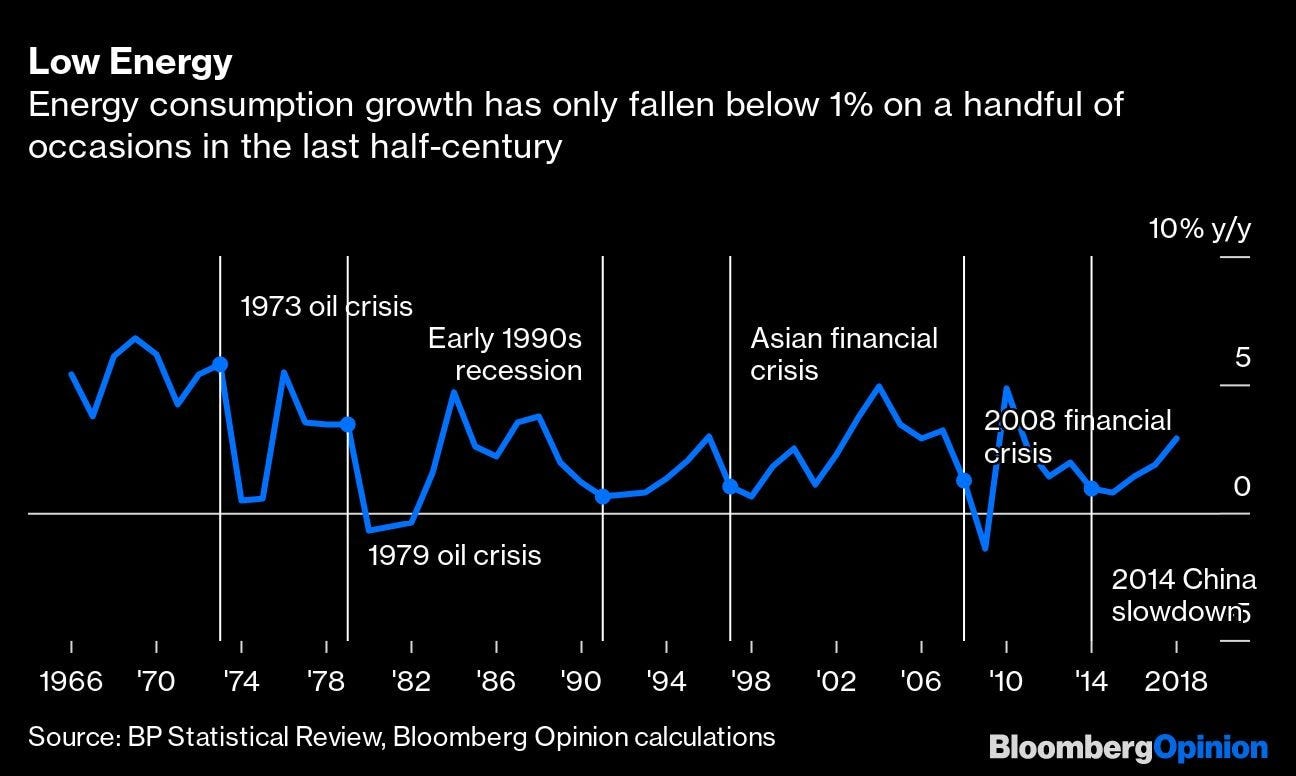

A key factor to bear in mind is that global downturns almost always throttle back energy consumption. There have only been six periods in the past half century when annual energy demand growth has fallen below 1% on a sustained basis, and four of them resulted from slowdowns like the one we currently seem to be witnessing.

That’s only going to be a temporary help, since recessions don’t so much slow the pace of emissions growth, as defer the pre-existing path for a few years. But there’s reason to think that this time really will be different. For one thing, unlike the solar panels that Jimmy Carter installed on the White House roof after the 1979 oil crisis, decarbonized alternatives are viable substitutes for fossil-fired energy now.

The 2020 oil crash will be remembered as a historical “gut check” on the strength and stickiness of the decarbonization movement. I’m betting that it’s pretty sticky. LINK

RESOURCES

The Keeling Curve a daily record of global atmospheric CO2 concentration.

Congressional Policy Tracker a summary of current federal energy legislation.

Click Clean your favorite apps and tech company clean power rankings.

Advancing Inclusion Through Clean Energy Jobs a report by the Brookings Institute.

Guide to Understanding the 5 Different Types of Electric Vehicles – read this before you buy or lease your next electric car.

Thanks for sharing your time with us!

If you enjoyed this newsletter but aren’t yet subscribed, sign up for a free subscription below.

If you are a subscriber, THANK YOU AGAIN, and please forward this to a friend.

👋 Questions, comments, advice? Send me an email!

Curated by Walter McLeod, Founder and Editor-in-Chief of Carbon Creed and Managing Partner with Eco Capitol Energy.